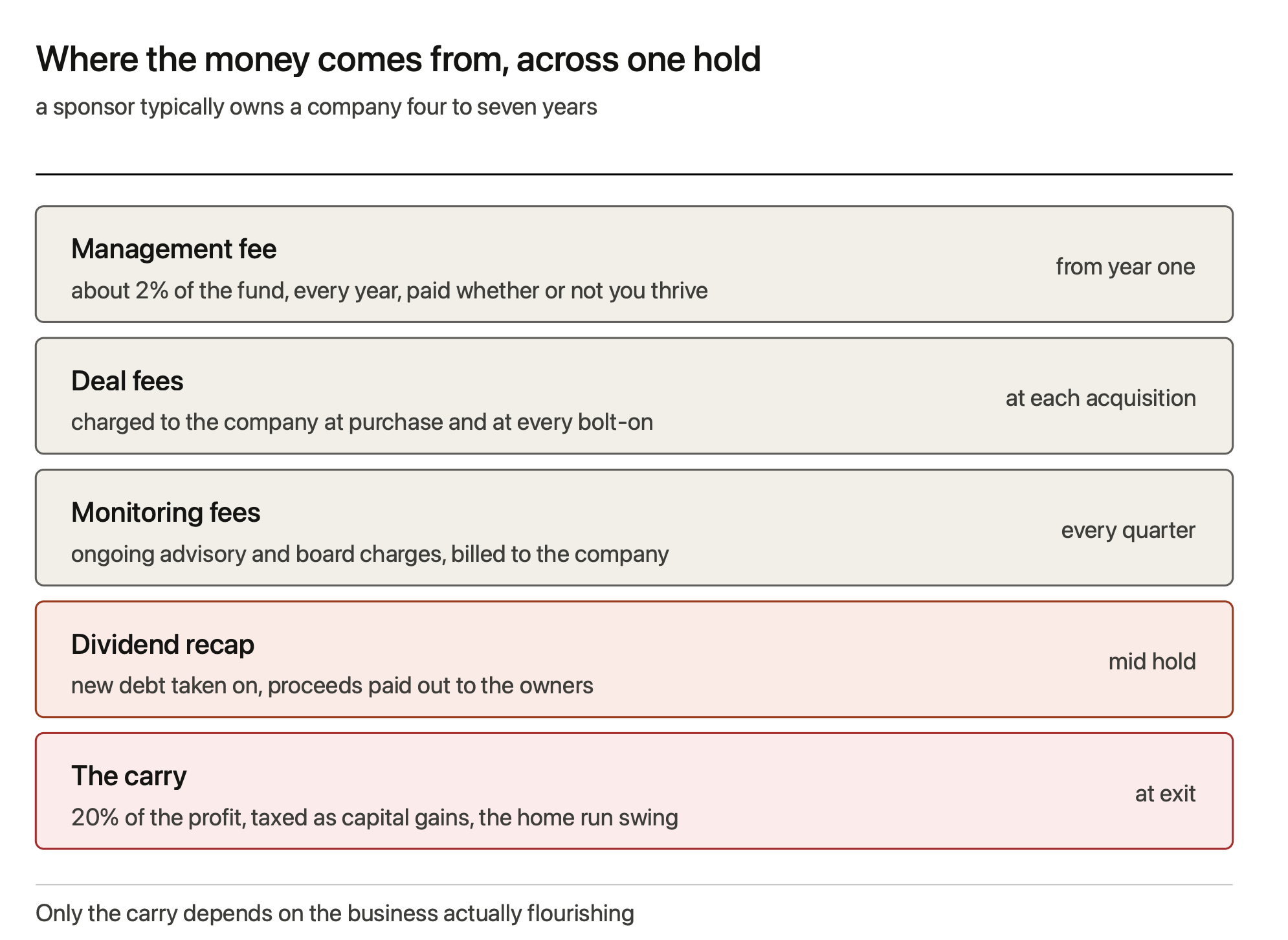

The Four Ways Private Equity Makes Its Money

Encore is going public. Behind the headline sits a lesson every events founder should learn before the next call from a sponsor.

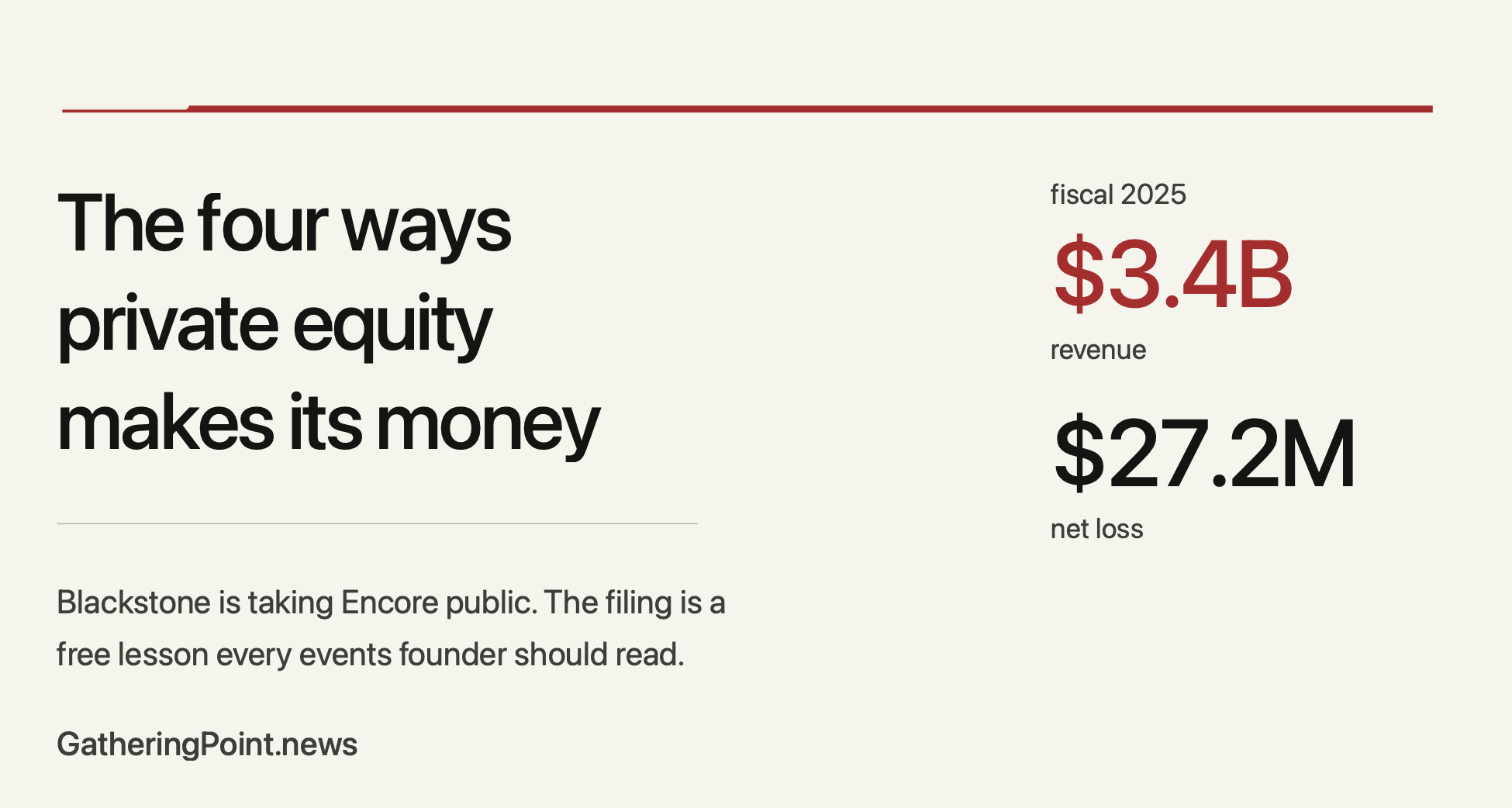

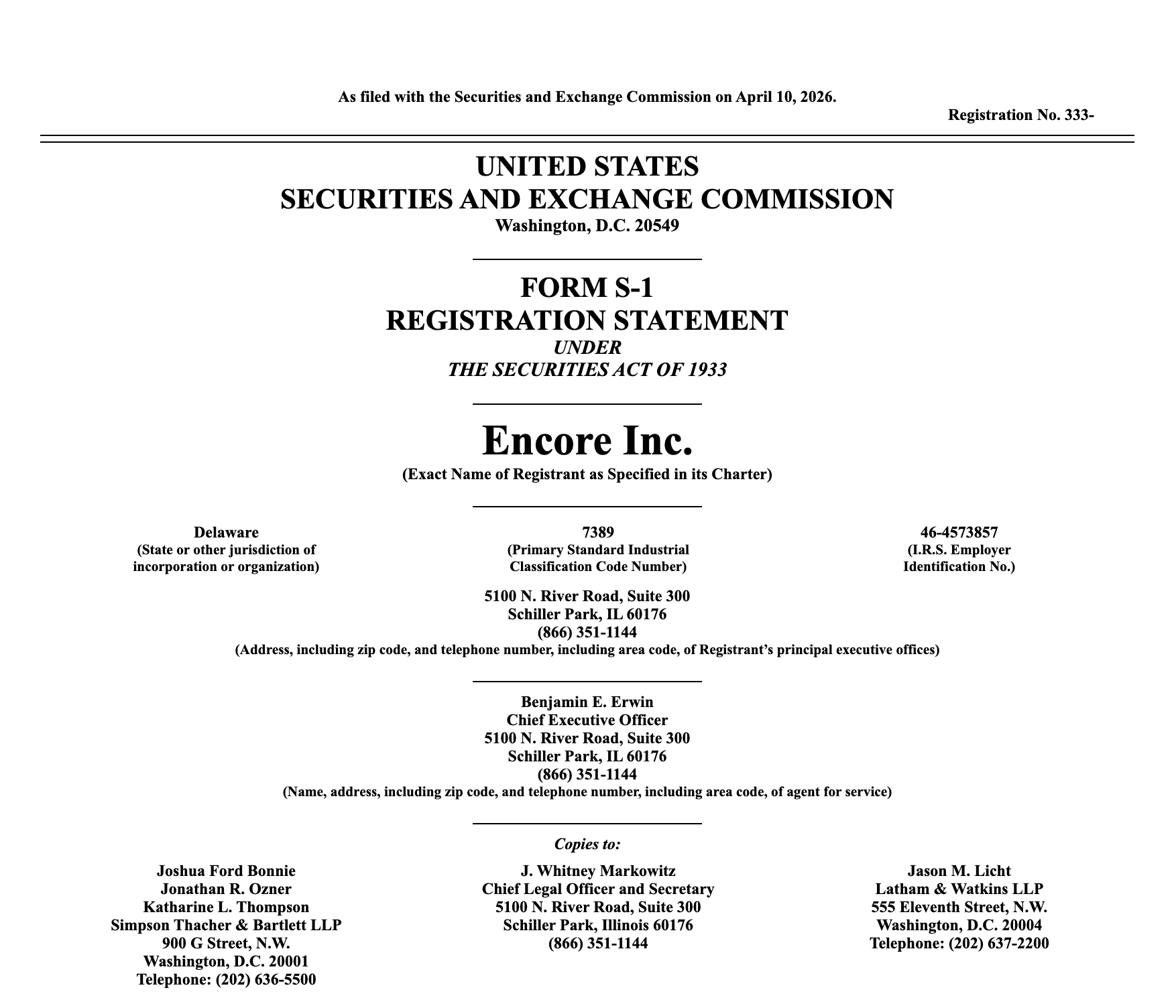

Blackstone bought PSAV in 2018, renamed it Encore in 2021, and has now filed to take it public on the New York Stock Exchange under the ticker ECR, seeking roughly $500 million. The company reported a net loss of $27.2 million on revenue of $3.4 billion for fiscal 2025, a sharp improvement on the $176.1 million loss on $3.2 billion the year before, and it intends to use the offering proceeds to repay debt and for general corporate purposes. For most of the meetings and events world the headline is simply that a giant is going public. The more useful story sits inside the filing, because the registration statement at the end of an eight-year private equity hold is the rarest of documents: a sponsor showing its work.

Founders tend to assume private equity makes money one way. Buy low, fix it up, sell high, pocket the difference. That is part of it. It is not most of it. A sponsor makes money on several layers at once, and only some of them depend on whether your company actually thrives. Once you see the layers, the entire posture of the firm across the table starts to make sense, and the events industry is now watching this play out across Encore, Clarion, Hyve, and the agency rollups being quietly assembled right now.

Here is how the money really flows.

One. The management fee.

A private equity firm does not invest its own money. It raises a fund from pension funds, university endowments, insurers, and increasingly wealthy individuals, then charges them an annual management fee, typically around two percent of committed capital. A firm overseeing ten billion dollars in committed capital earns two hundred million a year in fees alone, collected every year for the life of the fund, paid whether any single investment soars or sinks. This is the salary of the firm, and it arrives before a single dollar of profit has been made for anyone.

Two. The carry.

The performance fee, called carried interest or simply the carry, is twenty percent of the profits, paid to the firm after investors get their original money back plus a minimum return known as the hurdle rate, usually around eight percent. This is the home-run swing, and the reason the smartest people on Wall Street stay in private equity. It is also taxed at the long-term capital gains rate rather than as ordinary income, which means a managing director who takes home tens of millions in carry can pay a lower rate than the salaried people who work for him. Every administration has promised to close that loophole. None have.

Three. The deal fees.

When a sponsor buys a company, it often charges the company itself a transaction fee for the work of acquiring it. Then it charges another transaction fee on every bolt-on acquisition the company makes, plus ongoing monitoring and advisory fees billed quarter after quarter. This is why the people on a deal team are frequently rewarded for the size and volume of deals rather than the long-term success of them. The fees clear at closing. The success, if it comes, comes years later. Anyone who lived through the conglomerate buildups of the late twentieth century watched this dynamic warp decisions in real time, as assets were bought, starved, or sold according to what served the model rather than what served the business.

Four. The dividend recap.

This is the most elegant move in the business and the one founders least often see coming. Two or three years after the purchase, when lenders are willing, the company takes on a new and larger loan. The proceeds are not reinvested in growth. They are paid out as a dividend to the owners, chiefly the sponsor and its investors, who recover much of their original stake without selling a thing. Blackstone reportedly executed a private credit dividend recapitalization on Clarion Events in late 2025 reported in the range of one billion pounds, extracting returns while retaining ownership. The company emerges with more debt. The sponsor emerges with more cash.

What it means for the gathering economy.

Stack those four streams on top of one another and the picture clarifies. Management fees from year one. Deal fees at every acquisition. Monitoring fees every quarter. A dividend recap in the middle of the hold. And finally a sale or an IPO that crystallizes the carry. The firm wins on multiple layers, and several of those layers do not depend on whether the operating business flourishes. The company is being managed less for operating excellence than for the next transaction. The two overlap. They are not the same thing.

This is the lens to bring to the Encore filing. The improving loss, the revenue climbing toward three and a half billion, the expansion beyond hotels into corporate campuses through the Eclipse and FIRST acquisitions, the stated plan to use IPO proceeds to repay debt. All of it is the standard private equity construction reaching its natural conclusion: the operating business as collateral, leverage as the engine, the public offering as the release valve. Blackstone is the seller. The carry is being calculated. The cycle is closing exactly as designed.

For every founder in this industry being courted by a sponsor, the lesson is not that private equity is good or bad. It is that the people on the other side of the table run on a different financial physics than the people on your side of it. They make money in four ways. You make money in one. The deal can absolutely work for you, and many do. But it works only if you read the structure as carefully as they wrote it, before they send the letter of intent. The registration statement is on EDGAR. It is free. Anyone in this business who has never read one should read this one twice before the next phone call.

GatheringPoint covers the people who build the gatherings. Subscribe at GatheringPoint.news.