The Gathering Economy Is Now an Asset Class

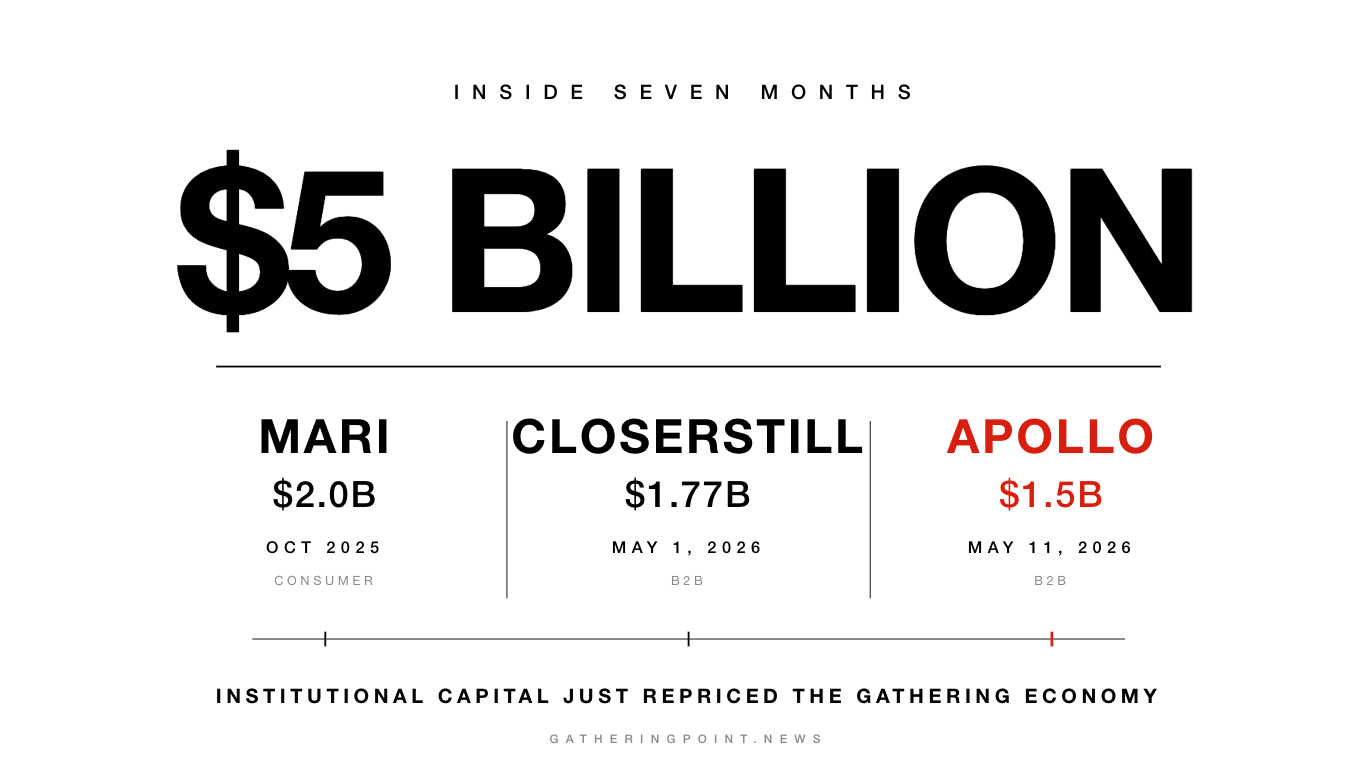

Apollo bought 140 trade shows. Searchlight bought CloserStill. MARI bought the consumer side. $5B, seven months. (113 chars, over) Tightened: Apollo, Searchlight, and MARI just spent $5 billion on live events in seven months.

Picture an independent conference organizer in Cleveland or Austin or Charlotte. She owns one good event in a vertical she knows well, maybe two if she has been at it long enough. She has fifteen employees, a venue contract she renegotiates every year, a sponsor list that took a decade to build, and a community Slack channel that lights up the week befo…